29 May 2026 • Reading Time:11min

Key Takeaways

- Standard homeowner’s insurance policies include firearms coverage, but the coverage limits are almost always far lower than collectors realize, typically capped at $1,500 to $2,500 for theft, with fire and other perils often covered under general personal property limits.

- Antique, collectible, and custom firearms are frequently undervalued or excluded entirely from standard policy payouts because the insurer uses replacement cost for a comparable modern firearm rather than actual market value.

- A scheduled firearms endorsement or a specialty collectibles policy provides coverage that matches the actual appraised value of each piece in the collection.

- Secure storage in a quality locked cabinet is a condition that affects whether a claim is paid and at what amount. Some policies specifically reduce or deny claims for firearms that were not stored in locked security.

- An accurate inventory with documented values, including photographs and appraisals, is required before a claim can be processed accurately. Most collectors do not have this documentation current.

- Insurance coverage and physical security are not substitutes for each other. Coverage addresses financial recovery after a loss. Physical security prevents the loss from occurring in the first place.

The Coverage Assumption That Costs Collectors Money

Most gun owners who carry homeowner’s or renter’s insurance believe their collection is covered. Technically, they are usually right. Most standard policies do include some coverage for firearms.

The problem is not the presence of coverage. It is the gap between what owners assume they have and what the policy actually provides.

A collector who has assembled a handgun collection worth $18,000 over the course of a decade, and who carries a standard homeowner’s policy with a $1,500 firearms theft limit, does not have $18,000 worth of coverage for that collection. They have $1,500. The other $16,500 of value exists in the collection but not in the policy.

This gap is not a bug in the insurance industry’s approach to firearms. It is the predictable result of buying coverage designed for households that own one or two firearms for home defense and not adjusting it for a collection that has grown significantly beyond that baseline.

This post explains how standard homeowner’s policies treat firearms, where the coverage gaps are most likely to appear, what options exist for closing those gaps, and what role proper storage plays in the insurance relationship.

Disclaimer: This post provides general information about how homeowner’s insurance typically treats firearms. It is not legal or insurance advice. Coverage terms vary significantly between insurers and policy types. Review your specific policy documents and consult your insurance agent or broker for guidance on your situation.

How Standard Homeowner’s Insurance Treats Firearms

Understanding the coverage framework requires understanding how homeowner’s insurance categorizes personal property.

Personal Property Coverage

Homeowner’s insurance includes personal property coverage, which protects the contents of a home against covered perils. Furniture, electronics, clothing, and most personal belongings fall under this coverage up to the policy’s overall personal property limit, which is typically set as a percentage of the home’s dwelling coverage.

Firearms are personal property and fall under this general coverage. However, most standard policies apply what are called “sublimits” to specific categories of property that are considered higher-risk for theft. Firearms are almost universally in a sublimit category.

The Firearms Sublimit

A sublimit is a cap within the broader personal property coverage. Even if the total personal property coverage on a policy is $100,000, the firearms sublimit might be $1,500 or $2,500 specifically for theft. If $30,000 worth of firearms is stolen, the policy pays the sublimit, not the full loss.

The most common firearms sublimits for theft in standard homeowner’s policies are:

- $1,500 is the most frequently cited limit in standard policies

- $2,500 appears in some policies and some states

- $5,000 is available in some higher-tier policies but requires specific selection

These figures represent the maximum payout for firearm theft under a standard policy, regardless of how many firearms were taken or what they were worth.

Fire and Other Perils

The sublimit structure for firearms typically applies specifically to theft. Fire, water damage, and other covered perils often fall under the general personal property coverage rather than the firearms sublimit, which means a loss from fire may be compensated differently than a loss from theft for the same collection.

This distinction matters but should not create false comfort. General personal property coverage uses “actual cash value” or “replacement cost” calculations that may still significantly undercompensate for collectible, antique, or custom firearms.

What “Replacement Cost” Actually Means for Collectibles

Standard policies that cover personal property at replacement cost calculate the payout based on what it would cost to purchase a comparable item new at current prices.

For a modern production firearm in a standard configuration, this calculation is straightforward. For an antique, a historically significant piece, a limited-production firearm, or one with documented provenance and collector premium, replacement cost for “a comparable item” does not reflect the actual market value of what was lost.

A Winchester Model 1894 produced in 1907 in excellent original condition cannot be replaced by purchasing a comparable Winchester at a retail store. The replacement cost calculation fails for this category of firearm in the same way it fails for any collectible whose value is determined by age, provenance, and condition rather than by production cost.

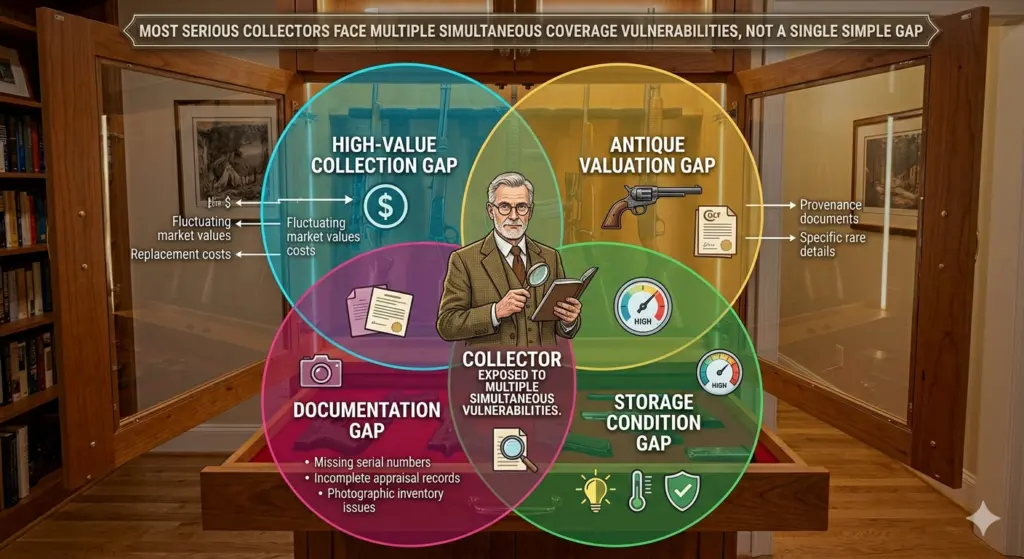

The Gaps Where Collectors Are Most Exposed

The High-Value Collection Gap

A collector who has spent five, ten, or twenty years building a meaningful collection has almost certainly outgrown the firearms sublimit in their standard policy without being aware of it. The collection grew gradually. The insurance coverage was set at inception and has not been reviewed against the collection’s current value.

This is the most common insurance exposure among serious collectors, and it is also the easiest to address once it is recognized.

The Antique and Collectible Valuation Gap

A standard policy’s replacement cost calculation does not assign value to rarity, age, provenance, or collector premium. An antique firearm with documented historical significance is worth significantly more to a collector than to a standard insurance calculation.

Without a specific scheduled endorsement or specialty policy that lists each piece at its appraised value, a claim involving antiques or significant collector pieces will be processed at standard replacement cost, which may represent a small fraction of actual market value.

The Documentation Gap

A claim can only be processed accurately for items that can be documented. A collector who cannot provide an accurate inventory with serial numbers, descriptions, photographs, and values is in a poor position to support a claim for the full value of a collection.

After a theft or fire, the documentation required to support an insurance claim must be assembled from memory and whatever records exist. For a collection that was never formally inventoried and appraised, this is difficult at best and potentially impossible for pieces whose provenance and value came from documentation that no longer exists.

The Storage Condition Gap

Some insurance policies include conditions related to how insured property was stored at the time of a loss. A policy that requires firearms to be kept in locked storage may reduce or deny a claim for a firearm that was not secured when it was stolen.

This is not universal. Policy language varies. But the possibility of a storage condition affecting a claim is a reason to review policy terms in detail and to maintain the storage practices that satisfy those terms regardless of whether a specific loss event has occurred.

Options for Closing the Coverage Gap

Scheduled Personal Property Endorsement (Rider)

A scheduled endorsement, sometimes called a scheduled rider or inland marine coverage, allows specific high-value items to be listed on a policy at their individually appraised value. Each listed item receives its own coverage limit equal to the documented value.

For firearms, this means listing each significant piece with its appraised value, serial number, and description. A stolen or damaged piece is compensated at the scheduled value, not at a sublimit or a standard replacement cost calculation.

Advantages:

- Coverage at actual appraised value for each listed piece

- Often provides coverage for a broader range of perils than the standard policy

- May include coverage for mysterious disappearance (an item that cannot be found) in addition to theft and damage

Considerations:

- Each scheduled item requires an appraisal, which has a cost

- The schedule must be updated as the collection grows or as values change

- Premiums increase with the total scheduled value

Specialty Firearms and Collectibles Insurance

Several insurers specialize in coverage for firearms collections, including collector-grade, antique, and high-value pieces. These policies are designed specifically for the collector market rather than adapted from standard homeowner’s coverage.

Specialty policies typically provide:

- Agreed value coverage, where the payout is a fixed agreed amount rather than a depreciated or replacement cost calculation

- Broader coverage for a wider range of perils

- Coverage for pieces in transit, at gun shows, or temporarily stored outside the home

- No sublimits that cap the total firearms coverage below the full collection value

For collectors with substantial collections, particularly those including antique or historically significant pieces, a specialty policy is typically the most appropriate coverage form.

Increasing the Standard Policy Sublimit

Some insurers offer the option to increase the firearms sublimit from the standard $1,500 or $2,500 to a higher amount, such as $5,000 or $10,000, through an endorsement. This is a partial solution for collectors whose collections are in the lower value range but does not address the antique valuation or documentation issues that affect higher-end collections.

The Inventory and Documentation You Need Before a Claim

The most important thing a gun owner can do for their insurance position, before any loss event, is to maintain a current and complete documented inventory of the collection.

An adequate firearms inventory for insurance purposes includes:

For each firearm:

- Make, model, and caliber or gauge

- Serial number

- Acquisition date and acquisition price (if known)

- Current appraised or estimated market value

- Description of any modifications, accessories, or special features that affect value

- Provenance documentation for antique or historically significant pieces

- Photographs from multiple angles showing current condition

The inventory as a whole:

- Total current value of the collection

- Date of the most recent appraisal for scheduled pieces

- Location where the inventory is stored (it must survive the same event that causes the loss, so a digital copy stored in cloud storage and a physical copy stored outside the home are appropriate)

Creating this documentation is a one-time effort that requires periodic updating as the collection changes. For collectors who have never done it, it is also the moment at which the actual value of the collection becomes clear and the gap between that value and existing coverage becomes visible.

What Secure Storage Means for Insurance

The relationship between storage quality and insurance coverage operates on several levels.

Policy Conditions

As noted, some policies specify storage conditions that affect coverage. A policy that requires firearms to be kept in locked security when not in use gives the insurer grounds to reduce or deny a claim for an unsecured firearm that was stolen. Reviewing the specific language of a policy’s storage requirements and satisfying those requirements consistently is the minimum standard.

Claim Credibility

A well-documented loss from a secure cabinet is more credible to an insurer than an undocumented loss from unsecured storage. A collector who can show that the collection was stored in a locked, quality cabinet, that the collection was inventoried and appraised, and that the storage was appropriate to the collection’s value presents a more credible claim than one who cannot demonstrate any of these things.

Prevention Is Better Than Recovery

The most important function of quality storage is not its effect on insurance claims. It is preventing the events that generate claims in the first place.

A handcrafted solid wood cabinet with a steel-reinforced locking bar, pick-resistant high-security locks, and bulletproof glass panels is not primarily an insurance tool. It is a security system designed to prevent unauthorized access. A collection that is never stolen does not need an insurance claim, regardless of how good the coverage is.

A locked, quality cabinet also significantly reduces the risk of theft because it makes the collection harder to access quickly. Most residential theft is opportunistic. A thief who encounters a quality cabinet in the available time is more likely to move on than to invest the time and tools required to defeat it.

The handcrafted gun cabinets and pistol chests built by Custom Cabinet Security are built with integrated steel-reinforced locking systems specifically designed to provide genuine physical security alongside their furniture quality. This is not a secondary consideration. It is a design priority from the beginning of each build.

Getting the Collection Appraised

A formal appraisal by a qualified firearms appraiser is the foundation of accurate insurance coverage and meaningful claim support.

When to Get an Appraisal

- When obtaining a scheduled endorsement or specialty policy (required for accurate coverage)

- When the collection includes antique, historically significant, or custom pieces whose value is not easily established by current retail pricing

- After acquiring any significant piece that meaningfully increases the total collection value

- Every three to five years for an active collection, since market values for collectible firearms change over time

- When estate planning requires establishing current fair market value for valuation purposes

What a Qualified Appraiser Provides

A professional appraisal from a qualified firearms appraiser documents the value of each piece using recognized market data, comparable sales, and the appraiser’s expertise in the specific categories of firearms being valued.

The resulting appraisal document is what the insurer uses to establish scheduled coverage amounts and what an estate uses to establish values for transfer purposes.

Qualified firearms appraisers may be located through gunsmith referrals, auction houses that handle collector firearms, or professional appraisal organizations. The appraiser’s qualifications and experience with the specific category of firearms being appraised matter. A general personal property appraiser may not have the expertise to accurately value antique or collectible firearms.

A Practical Coverage Review Checklist

For a gun owner who has never reviewed their firearms coverage against their actual collection, this checklist identifies the most important steps.

Step 1: Pull the current policy documents and find the firearms sublimit. Read the exact language. Note the theft sublimit and any language about covered perils, storage conditions, and valuation methods.

Step 2: Compare the sublimit to the estimated current value of the collection. If the collection value is materially higher than the sublimit, the gap is real and requires action.

Step 3: Identify any antique, collectible, or custom pieces. These are the items most likely to be undervalued by a standard replacement cost calculation and most in need of scheduled or specialty coverage.

Step 4: Assess the current inventory documentation. Is there a current, complete list with serial numbers and photographs? If not, create one before any other coverage changes are made. The documentation is required to support any claim and to establish scheduled values.

Step 5: Contact an insurance agent or broker. Specifically ask about scheduled personal property endorsements for firearms and whether specialty firearms policies are available through the agency. Compare the cost and coverage of increasing the standard sublimit, adding a scheduled endorsement, and a standalone specialty policy.

Step 6: Review the storage conditions in the policy. Ensure the current storage meets any policy requirements. If it does not, update the storage approach before the coverage conversation is concluded.

Step 7: Schedule an appraisal for significant pieces. For any piece where the replacement cost calculation would not accurately reflect actual value, a formal appraisal is required before scheduled coverage can be obtained at the correct value.

The Insurance and Storage Relationship in Plain Terms

Insurance and storage address different aspects of the same underlying concern: protecting a collection from loss.

Insurance addresses financial recovery after a loss has occurred. If a collection is stolen or damaged despite the best security measures, appropriate coverage ensures the financial value of that collection is not simply gone.

Storage and physical security address prevention. A quality cabinet with genuine security features reduces the probability that a theft or unauthorized access event occurs in the first place.

Both are necessary. Neither substitutes for the other.

A collector who has excellent insurance but inadequate physical security is relying on financial recovery after a loss that could have been prevented. The loss of a historically significant piece, a family heirloom, or a piece with personal meaning cannot be fully compensated by any insurance payout, regardless of coverage amount.

A collector who has excellent physical security but inadequate insurance is protected against most loss events but is fully exposed to financial loss if those security measures are defeated.

The right approach is quality storage that prevents most loss events, and appropriate insurance coverage that addresses the financial impact of the events that cannot be prevented.

The custom consultation process at Custom Cabinet Security is a conversation about the physical security side of this equation. The craftsmen in Arthur, Illinois build cabinets with integrated security systems because security and craftsmanship are not competing priorities. They are both part of what makes a handcrafted gun cabinet worth owning.

The Bottom Line

Most gun owners have meaningful coverage gaps between what their standard homeowner’s policy provides and what their collection is actually worth. The gap is widest for collectors with high-value collections, antique or historically significant pieces, and inadequate documentation.

Closing that gap requires reviewing the actual policy language, understanding the sublimit structure, documenting the collection accurately, and obtaining coverage appropriate to the actual value of what is owned. For most collectors, this means either a scheduled endorsement or a specialty firearms policy rather than the standard policy as written.

Physical security is the complement to insurance, not a substitute for it. A quality handcrafted cabinet with genuine security features reduces the likelihood that coverage ever needs to be claimed. Appropriate insurance coverage ensures that if it does, the financial recovery reflects the actual value of what was lost.

Both decisions deserve the same attention from any collector who has built something worth protecting.

Related Posts

View All

Uncategorized

Reading Time:11min

Custom Gun Safe vs. Off-the-Shelf Safe: Is Handcrafted Worth It for a Serious Collector?

Key Takeaways The Question Worth Asking Honestly “Is handcrafted worth it” is a question that deserves a direct answer, not

Read More

Uncategorized

Reading Time:16min

How to Control Humidity Inside a Wood Gun Cabinet (And Why It Matters for Your Firearms and the Wood Itself)

Key Takeaways The Problem That Never Announces Itself The most damaging thing that happens inside an improperly maintained gun cabinet

Read More

Uncategorized

Reading Time:11min

Pistol Display Cases vs. Gun Cabinets: Which Storage Solution Fits a Mixed Collection?

Key Takeaways The Storage Problem That Grows With the Collection Most gun collections do not start as mixed collections. A

Read More